Navigating the Investment Landscape:

A Comprehensive Guide to Types and Their Aspects

Introduction:

In today's dynamic financial world, the concept of "investment" extends far beyond traditional savings accounts. It encompasses a vast universe of opportunities, each with its own characteristics, risks, and potential rewards.

Section 1:

Stocks (Equities) - The Engine of Growth

Stocks, also known as equities, represent fractional ownership in a company.

Aspects of Stocks:

Potential for Capital Appreciation: This is the primary draw of stock investing. If the company performs well, grows its business, and increases its profitability, the market value of its stock is likely to increase, allowing you to sell your shares for more than you paid for them.

This can generate significant returns over the long term. Dividends: Many companies distribute a portion of their profits to shareholders in the form of dividends. These are typically paid quarte

rly, though some companies pay monthly, semi-annually, or annually. Dividends provide a regular income stream and can be reinvested to buy more shares, further accelerating wealth accumulation through compounding. Volatility and Risk: Stocks are generally considered more volatile than other asset classes like bonds.

Their prices can fluctuate significantly in short periods due to company-specific news, industry trends, economic indicators, geopolitical events, or overall market sentiment. This volatility translates to higher risk; there's no guarantee that a stock's value will increase, and you could lose a portion or even all of your initial investment. Liquidity: Most publicly traded stocks are highly liquid, meaning they can be bought and sold relatively easily on exchanges during market hours.

This allows investors to access their capital quickly if needed. Types of Stocks:

Growth Stocks: Companies expected to grow earnings and revenues at a faster pace than the overall market.

Often reinvest profits back into the business rather than paying dividends. (e.g., tech companies, innovative startups). Value Stocks: Companies that are perceived to be undervalued by the market, often trading at a lower price relative to their earnings or assets.

May offer regular dividends. (e.g., mature industrial companies, utilities). Income Stocks: Companies that consistently pay high dividends, often mature and stable businesses.

(e.g., real estate investment trusts (REITs), utility companies). - Blue-Chip Stocks: Large, well-established, financially sound companies with a long history of stable earnings and reliable dividends.

(e.g., Apple, Microsoft, Johnson & Johnson).

Company Performance: Earnings reports, revenue growth, profit margins, and new product announcements are fundamental drivers.

Economic Outlook: Strong GDP growth, low unemployment, and controlled inflation generally support higher stock prices. Conversely, fears of recession (a topic of discussion in mid-2025 for some economies due to persistent inflation and high interest rates) can depress market sentiment.

Interest Rates: In a higher interest rate environment (as seen in some major economies in 2025), borrowing costs for companies increase, which can impact profitability.

Also, higher interest rates make fixed-income investments more attractive, potentially drawing money away from stocks. Inflation: While some inflation is normal, high and persistent inflation can erode corporate profits and consumer purchasing power, negatively impacting stock performance.

However, some companies are better positioned to pass on costs. Geopolitical Events: Trade tensions (e.g., US-China, US-EU tariffs remain a hot topic), conflicts, and political instability can introduce significant market volatility.

Technological Advancements: Sectors like AI, renewable energy, and biotech are experiencing rapid innovation, leading to significant opportunities (and risks) for related stocks.

Section 2:

Bonds (Fixed Income) - The Pillar of Stability and Income

Definition: Bonds are debt instruments, essentially a loan made by an investor to a borrower (typically a corporation or government). When you buy a bond, you are lending money to the issuer

Aspects of Bonds:

Regular Income Stream (Interest Payments): The primary appeal of bonds is the predictable income they provide. Bond issuers pay a fixed interest rate, known as the "coupon rate," at specified intervals (e.g., semi-annually, annually). This makes them attractive for investors seeking stable cash flow.

Lower Volatility and Risk (Relative to Stocks): Bonds are generally considered less volatile and less risky than stocks. This is because they have a defined maturity date and the promise of principal repayment, making their price movements less dramatic. However, bonds are not risk-free.

Capital Preservation: Bonds are often used to preserve capital, especially for investors nearing retirement or those with a lower risk tolerance. The promise of getting the principal back at maturity provides a sense of security.

Liquidity: The liquidity of bonds varies significantly. Highly liquid government bonds (like U.S. Treasuries or Indian Government Bonds) can be traded easily. Corporate bonds, especially those from smaller issuers, might be less liquid, making them harder to sell quickly without impacting the price.

Types of Bonds:

Government Bonds: Issued by national governments (e.g., U.S. Treasury bonds, Gilts in the UK, G-Secs in India). Generally considered the safest due to the backing of the issuing government's taxing power.

Corporate Bonds: Issued by companies to raise capital. Carry higher risk than government bonds but offer potentially higher yields to compensate for the increased credit risk.

Municipal Bonds (Munis): Issued by state and local governments. In some countries (like the U.S.), the interest earned on Munis can be tax-exempt at federal, state, and local levels, making them attractive to high-income investors.

High-Yield Bonds (Junk Bonds): Issued by companies with lower credit ratings. They offer much higher interest rates to compensate for the significantly greater risk of default.

Inflation-Protected Securities (e.g., TIPS): Bonds whose principal value adjusts with inflation, protecting investors from the erosion of purchasing power.

Key Bond Risks:

Interest Rate Risk: This is the most significant risk for bondholders. When market interest rates rise, the value of existing bonds (especially those with lower fixed coupon rates) typically falls because newly issued bonds offer higher yields, making older bonds less attractive. Conversely, when rates fall, existing bond values tend to rise. In mid-2025, with many central banks calibrating policy, this risk remains pertinent.

Credit Risk (Default Risk): The risk that the bond issuer may not be able to make its interest payments or repay the principal. This risk is higher for corporate bonds and high-yield bonds than for government bonds. Credit ratings (e.g., from Moody's, S&P, Fitch) help assess this risk.

Inflation Risk: The risk that inflation will erode the purchasing power of your bond's future interest payments and principal repayment, particularly for long-term bonds with fixed coupons.

Reinvestment Risk: The risk that when a bond matures or is called (paid back early), you may have to reinvest the proceeds at a lower interest rate, particularly in a falling rate environment.

Suitability: Bonds are suitable for investors seeking stable income, capital preservation, and lower risk exposure than stocks. They are crucial for portfolio diversification, helping to cushion against stock market downturns. Bonds are particularly attractive for investors with a moderate to low-risk tolerance, those nearing retirement, or those building the fixed-income portion of a balanced portfolio. In an environment where global central banks are either holding rates steady or contemplating cuts (as is the case for some in mid-2025), the yields offered by bonds can be quite attractive compared to a few years prior, though rising inflation concerns can still temper returns for some.

Section 3:

Mutual Funds and Exchange-Traded Funds (ETFs) - Diversification at Your Fingertips

Definition: Mutual Funds and Exchange-Traded Funds (ETFs) are popular investment vehicles that allow individual investors to pool their money with other investors to collectively buy a diversified portfolio of stocks, bonds, or other securities. Instead of buying individual securities, you buy shares of the fund, which then owns the underlying assets. They are managed by professional fund managers.

Mutual Funds:

Definition: A mutual fund is a type of professionally managed investment fund that gathers money from many investors to purchase securities. The fund's portfolio is structured and maintained to match the investment objectives stated in its prospectus.

Aspects of Mutual Funds:

Professional Management: Fund managers conduct research, select securities, and continuously monitor the portfolio. This is a significant advantage for investors who lack the time, expertise, or desire to manage their own portfolios.

Diversification: By investing in a mutual fund, you instantly gain exposure to a wide range of securities, even with a small investment. This inherent diversification significantly reduces idiosyncratic risk (risk associated with a single security).

Accessibility: Mutual funds make it easy for small investors to access diverse portfolios that would otherwise require substantial capital.

Variety: There's a vast array of mutual funds catering to various investment objectives, risk tolerances, and asset classes (e.g., equity funds, debt funds, balanced funds, sector-specific funds, international funds).

Pricing: Mutual funds are typically priced once a day, at the end of the trading day, based on their Net Asset Value (NAV). When you place an order, you buy or sell at the next calculated NAV.

Costs: Mutual funds typically charge various fees, including:

Expense Ratio: An annual fee charged as a percentage of your investment to cover management fees, administrative costs, and other operational expenses.

Load Fees: Some funds charge a "load" (sales commission) – either a front-end load (paid when you buy) or a back-end load (paid when you sell). "No-load" funds do not charge sales commissions.

Suitability: Mutual funds are excellent for long-term investors seeking professional management, diversification, and convenience. They are suitable for beginners and experienced investors alike, offering a way to achieve broad market exposure without active management on their part.

Exchange-Traded Funds (ETFs):

Aspects of ETFs:

Real-Time Trading: A key differentiator from mutual funds is that ETFs can be bought and sold throughout the trading day, offering greater flexibility and liquidity.

Lower Costs: ETFs generally have lower expense ratios compared to actively managed mutual funds, primarily because many are passively managed, tracking an index rather than trying to outperform it.

Diversification: Like mutual funds, ETFs offer instant diversification by holding a basket of securities.

Transparency: Most ETFs disclose their holdings daily, providing investors with complete transparency into what they own.

Tax Efficiency: ETFs are often more tax-efficient than mutual funds due to their unique creation/redemption mechanism, which minimizes capital gains distributions to shareholders.

Variety: The ETF market has exploded, with ETFs tracking virtually every imaginable index, sector, commodity, or investment strategy (e.g., S&P 500 ETFs, sector-specific ETFs, bond ETFs, gold ETFs).

Brokerage Commissions: While ETFs have lower expense ratios, you typically pay a brokerage commission when you buy or sell ETF shares, similar to trading individual stocks. However, many brokers now offer commission-free ETF trading.

Suitability: ETFs are suitable for a wide range of investors, from those seeking broad market exposure at low cost to those pursuing specific sector or thematic investments. Their real-time trading ability also appeals to active traders, though their long-term benefits are most pronounced for buy-and-hold investor.

:max_bytes(150000):strip_icc()/EFT_final-45a9ca8cf7e948608a3b8dae38b66393.png)

In mid-2025, both mutual funds and ETFs remain highly popular. ETFs continue to gain market share due to their lower costs, tax efficiency, and intraday trading flexibility, especially as passive investing strategies grow in prominence amid global economic uncertainties. However, actively managed mutual funds still appeal to investors who believe in the ability of skilled managers to outperform benchmarks, particularly in niche or less efficient markets. The choice often comes down to cost, trading flexibility, and whether you prefer active vs. passive management.

Section 4:

Real Estate and Alternative Investments - Beyond Traditional Markets

As investors seek further diversification and potentially higher returns, or opportunities uncorrelated with traditional stock and bond markets, they often look towards real estate and a broader category known as "alternative investments." These assets typically involve different risk profiles, liquidity characteristics, and investment horizons.

Real Estate:

Definition: Real estate investment involves the purchase, ownership, management, and/or sale of property for profit. This can include residential, commercial, industrial, or land properties.

Aspects of Real Estate Investment:

Tangible Asset: Unlike stocks or bonds, real estate is a physical asset that you can see and touch. This tangibility can provide a sense of secur

1 ity for many investors.Income Generation (Rent): Many real estate investments generate regular income through rental payments from tenants. This consistent cash flow can be a significant draw.

Potential for Appreciation: Property values can increase over time due to factors like economic growth, population increase, infrastructure development, and inflation.

Leverage: Investors can often finance a significant portion of a real estate purchase with borrowed money (mortgages). While this can amplify returns, it also amplifies risk.

Inflation Hedge: Real estate is often considered a good hedge against inflation. As the cost of living rises, so too do property values and rental income, maintaining purchasing power.

Diversification: Real estate often has a low correlation with traditional stock and bond markets, meaning its performance doesn't always move in sync with them, offering valuable diversification benefits.

Illiquidity: This is a major disadvantage. Selling real estate can be a lengthy process (weeks or months), making it difficult to access your capital quickly.

High Transaction Costs: Buying and selling property involves significant costs, including agent commissions, legal fees, taxes, and appraisal fees.

Management Demands: Direct property ownership can be time-consuming and require active management (maintenance, tenant issues, legal compliance).

Ways to Invest:

Direct Ownership: Buying physical properties (residential homes, commercial buildings).

Real Estate Investment Trusts (REITs): Companies that own, operate, or finance income-generating real estate. They trade on stock exchanges like stocks, providing a more liquid way to invest in real estate and often pay high dividends.

Real Estate Crowdfunding: Pooling money with other investors online to invest in specific real estate projects.

Real Estate Mutual Funds/ETFs: Funds that invest in portfolios of real estate companies or REITs.

Suitability: Real estate is suitable for investors with a long-term horizon, who are comfortable with illiquidity and potentially high upfront capital requirements (for direct ownership). REITs offer a more liquid and less capital-intensive way for almost any investor to gain real estate exposure. In mid-2025, while some commercial real estate segments face headwinds (e.g., office spaces due to remote work), residential real estate in many areas remains robust, and sectors like data centers and logistics are seeing strong demand.

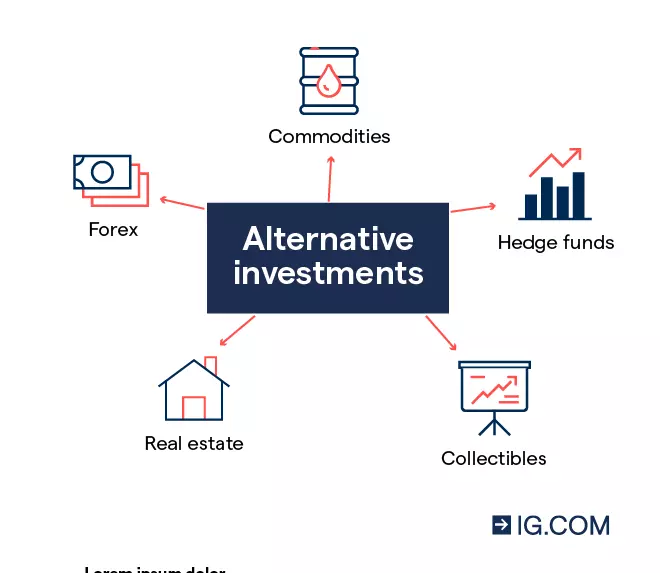

Alternative Investments:

Definition: Alternative investments are asset classes that fall outside of traditional investments like stocks, bonds, and cash. They are typically less liquid, more complex, and often require a higher minimum investment, making them historically more accessible to institutional investors or high-net-worth individuals. However, democratized access is growing.

Aspects of Alternative Investments:

Diversification: Their low correlation with traditional assets is a primary driver, helping to reduce overall portfolio volatility.

Potential for Higher Returns: Many alternatives aim for absolute returns regardless of market conditions or seek to capitalize on unique opportunities, potentially offering higher returns than traditional assets, though often with higher risk.

Illiquidity: Most alternative investments are highly illiquid, meaning they cannot be easily converted to cash.

Complexity and Due Diligence: They often involve complex structures and require significant expertise for proper evaluation.

Less Regulation: Some alternative investments may have less regulatory oversight compared to public markets.

Types of Alternative Investments (Brief Overview):

Private Equity: Investing in private companies not listed on a public exchange. This can involve venture capital (early-stage companies) or leveraged buyouts (mature companies).

Hedge Funds: Investment funds that use a variety of sophisticated strategies, including leveraging and short-selling, to generate high returns. Often have high minimums and limited liquidity.

Commodities: Raw materials such as gold, silver, oil, natural gas, agricultural products. Can be volatile but act as an inflation hedge.

Derivatives: Financial instruments whose value is derived from an underlying asset (e.g., futures, options). Used for hedging or speculation, highly complex and risky.

Collectibles: Art, rare coins, stamps, wine, classic cars. Their value is driven by supply and demand and aesthetic appeal. Very illiquid and specialized.

Infrastructure: Investments in essential public services and facilities, like roads, bridges, utilities, and airports. Offers stable, long-term cash flows.

Structured Products: Custom-tailored financial instruments designed to meet specific investor needs, often combining features of different asset classes.

Suitability: Alternative investments are generally suitable for sophisticated investors with significant capital, a high-risk tolerance, a long-term horizon, and no immediate need for liquidity. They are typically used to enhance diversification and potentially boost returns in a well-established portfolio, often forming a smaller percentage of overall holdings. In mid-2025, interest in alternatives remains high as investors seek yield and diversification outside of potentially overvalued public markets, with private credit and infrastructure funds seeing particular interest.

Conclusion: Crafting Your Investment Journey

Embarking on the investment journey is a crucial step towards achieving your financial aspirations, whether they involve funding retirement, purchasing a home, or simply building wealth. As we've explored, the world of investments is incredibly diverse, offering a spectrum of options from the growth potential of stocks and the stable income of bonds to the accessible diversification of mutual funds and ETFs, and the unique opportunities found in real estate and alternative investments.

No single investment type is universally "best." Instead, the optimal strategy lies in creating a diversified portfolio tailored to your individual circumstances. This means carefully considering several key factors:

Your Financial Goals: What are you saving for, and when do you need the money? Short-term goals might favor lower-risk assets, while long-term objectives can accommodate more volatility.

Your Risk Tolerance: How comfortable are you with the possibility of losing money in exchange for potentially higher returns? Understanding your comfort level with market fluctuations is paramount.

Your Time Horizon: How long do you plan to invest? Longer horizons generally allow you to ride out market downturns and benefit from compounding returns.

Liquidity Needs: How quickly might you need access to your invested capital? Some assets are far more liquid than others.

Current Economic Climate: As we've seen with the mid-2025 context, factors like interest rates, inflation trends, and global trade dynamics can influence the attractiveness and performance of different asset classes. Staying informed and adapting your strategy as conditions evolve is part of smart investing.

Ultimately, successful investing is not about picking the "hottest" trend but about building a well-researched, balanced portfolio that aligns with your unique financial DNA. It requires ongoing learning, patience, and often, the discipline to stick to your plan even when markets are turbulent. By understanding the fundamental aspects of various investment types, you're empowered to make informed decisions, mitigate risks, and confidently navigate the dynamic investment landscape on your path to financial well-being.

Comments

Post a Comment